The Simple Method That's Helping People Pay Off Credit Card Debt in 30 Days — Without a Single Spreadsheet

You check your bank balance before you even get out of bed.

Please let it be more than I think it is.

It's not.

You make decent money. You know you do. Your friends think you're doing fine. Your family definitely thinks you're doing fine.

So why does it feel like the money disappears the second it lands?

Where does it even go?

You've tried to figure it out. Budgeting apps you deleted after two weeks. A spreadsheet you opened once and never again. That one YouTube video everyone swears by.

None of it stuck. Not because you're lazy. Not because you're bad with money. Because none of it was built for someone who's already mid-spiral.

You're tired of feeling like this is just who you are with money.

You're tired of doing quiet math in your head before every purchase.

Can I actually afford this, or am I just going to feel sick about it later?

Drop everything you're doing right now, and read every word of what I'm about to share.

Where This Actually Comes From

I want to be straight with you before we go any further: there's no secret mentor, no mystery ritual, no chance encounter at a family gathering where someone handed me an old formula. I'm not going to invent one, because you'd see through it anyway — and you deserve better than that.

What actually happened is less dramatic and more useful. I spent a long time looking at why so many financially literate, hardworking people still end up exactly where you are right now. Not broke from bad decisions. Broke from invisible ones.

Why the Usual Advice Doesn't Work

You've probably already tried the standard fixes. A budgeting app that wanted you to categorize every transaction by hand — until life got busy and you stopped opening it. A spreadsheet that worked for exactly one month. A raise that, somehow, got absorbed within a few weeks and left you no further ahead than before. Maybe you've avoided checking your statements altogether, because not looking feels safer than looking and seeing the number.

None of these failed because you didn't try hard enough. They failed because they all assume the same thing: that the problem is a lack of information. It isn't. You already know, roughly, where your money goes. The problem is that knowing isn't the same as having a system that catches the leak before it happens, not after.

What Actually Breaks the Cycle

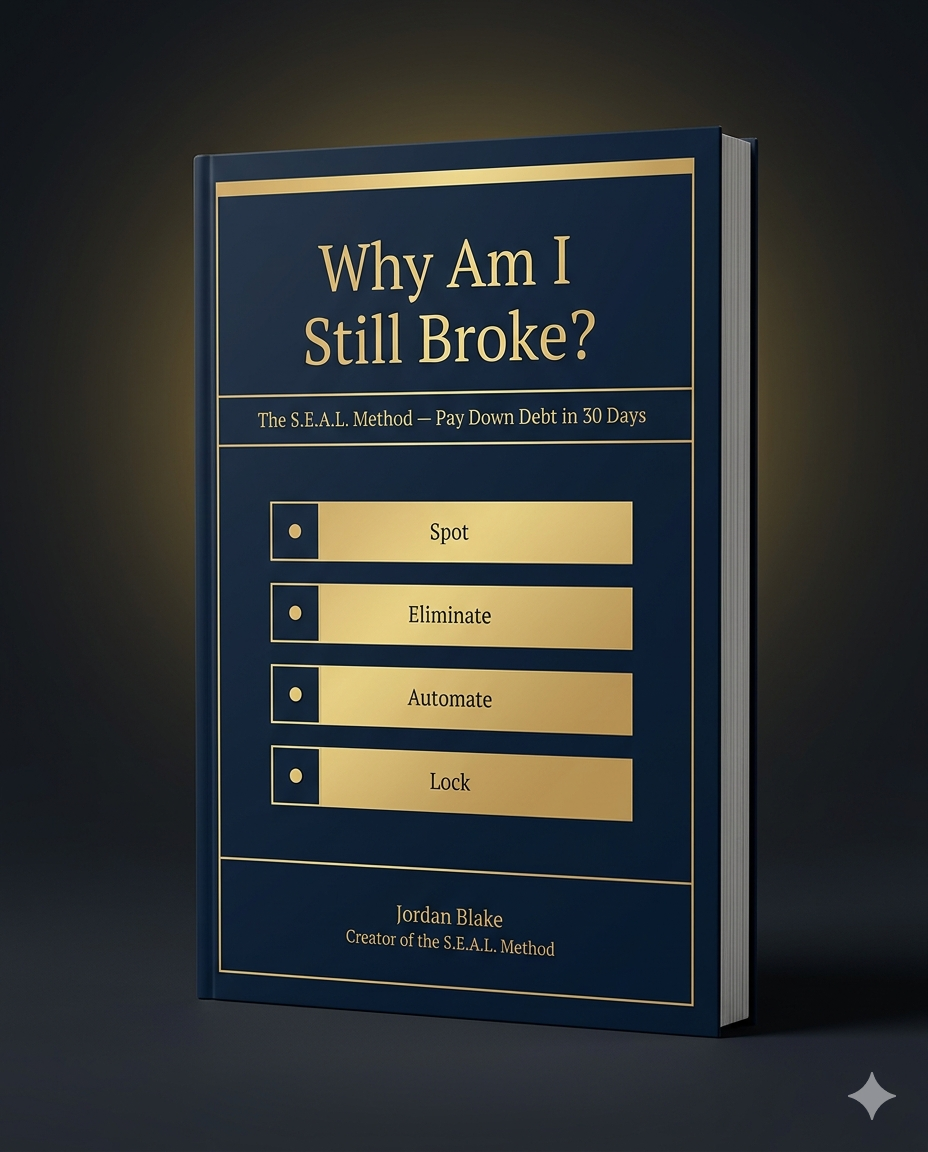

That's the gap the S.E.A.L. Method is built to close. Four moves, in order:

Spot the leak — a short audit that shows you exactly where the money is actually going, not where you assume it's going.

Eliminate the trigger — the specific moment that causes the spending, named and interrupted, instead of relying on willpower in the moment.

Automate the payoff — money moves toward your debt before it has a chance to disappear somewhere else.

Lock in the buffer — a small cushion so one unexpected bill doesn't undo a month of progress.

None of these steps require you to be good with money. They just require you to follow the order.

What Tends to Change Once It Clicks

The relief isn't really about the dollar amount at first. It's about opening a banking app without that flinch. It's being able to answer "where did it go" instead of shrugging.

It can change the conversation with a partner, too — not because the number magically gets smaller, but because having an answer instead of an excuse tends to make that conversation a little less tense.

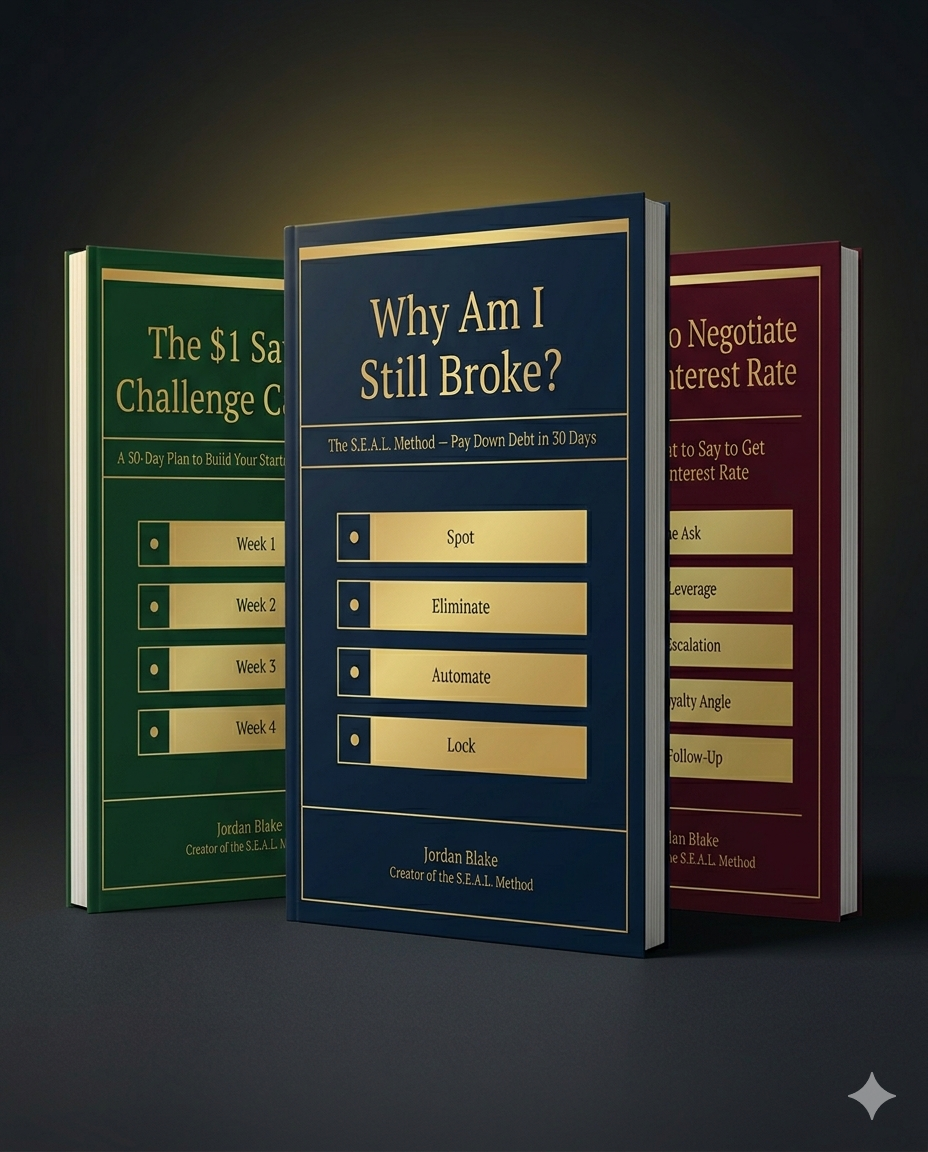

I kept getting asked for the exact steps, in order, with the actual worksheets — so I packaged everything into one simple guide.

The full method, the worksheets, the exact order to follow it in, and how to know it's actually working.

Introducing —

Inside this guide, you'll find:

- The Money Leak Audit — find exactly where your money is going in 15 minutes, no spreadsheet required. — Pg. 4

- The full S.E.A.L. framework — explained simply, in the order you actually use it. — Pg. 7

- The Spending Trigger Journal — name the exact moments that lead to off-plan spending. — Pg. 12

- The Pay-Yourself-First setup guide — automate the payoff so it happens before the money disappears. — Pg. 16

- The Debt Payoff Tracker — a visual way to actually watch the number move. — Pg. 20

- The Emergency Buffer Calculator — figure out the smallest cushion that actually protects your progress. — Pg. 24

- The 30-Day Checklist — exactly what to do, day by day. — Pg. 27

And the best part? You don't need a finance degree, hours of spreadsheet work, or to feel ashamed asking for help. It's the same simple method, broken down so you can actually follow it.

What This Actually Costs You

This costs less than one month's interest on a $5,000 balance at today's typical 24% credit card APR — about $100 — and it's built to help you stop paying that every single month.

WAIT! Two Free Gifts For You (Today Only)

If you're among the first 100 buyers, you'll get these bonuses included at no extra cost.

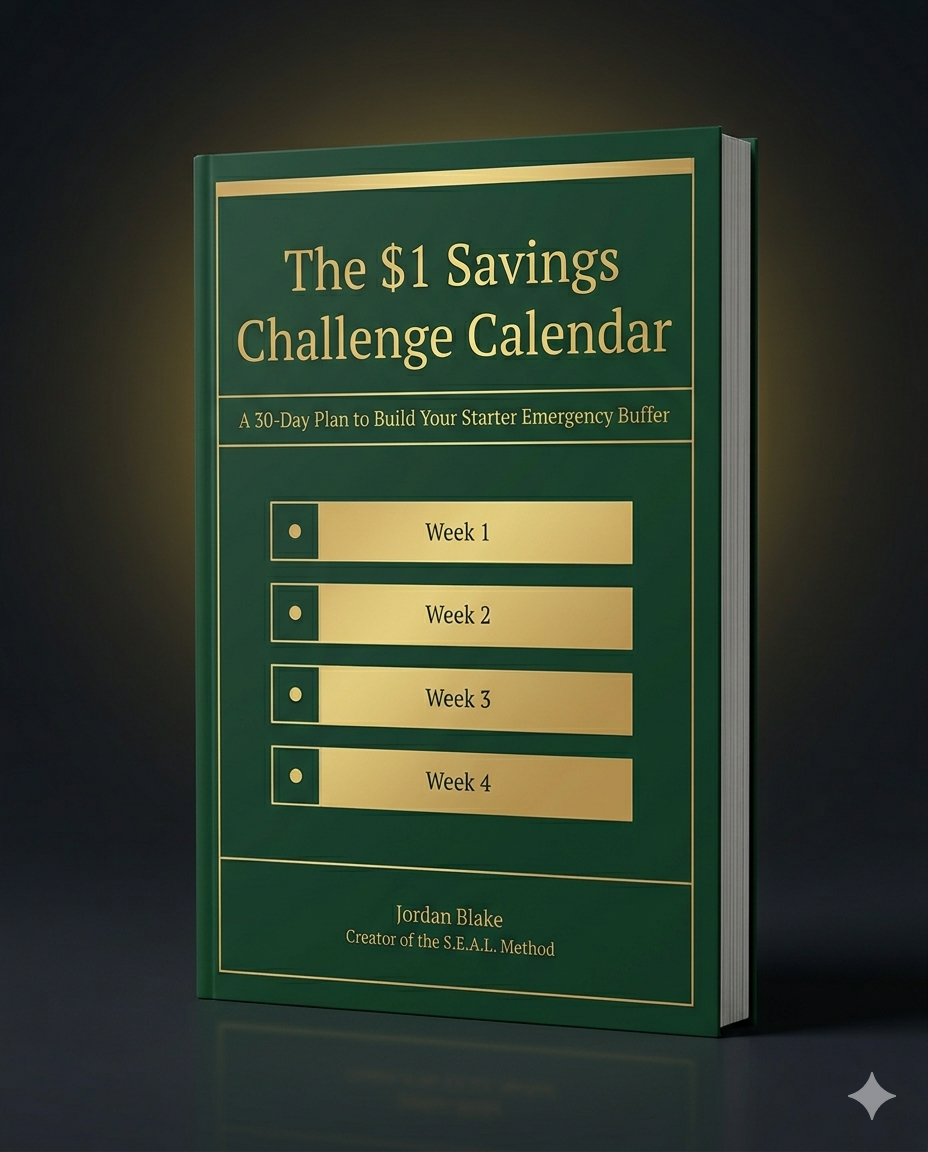

Bonus 1: The $1 Savings Challenge Calendar

A 30-day printable that builds a starter emergency buffer one small step at a time.

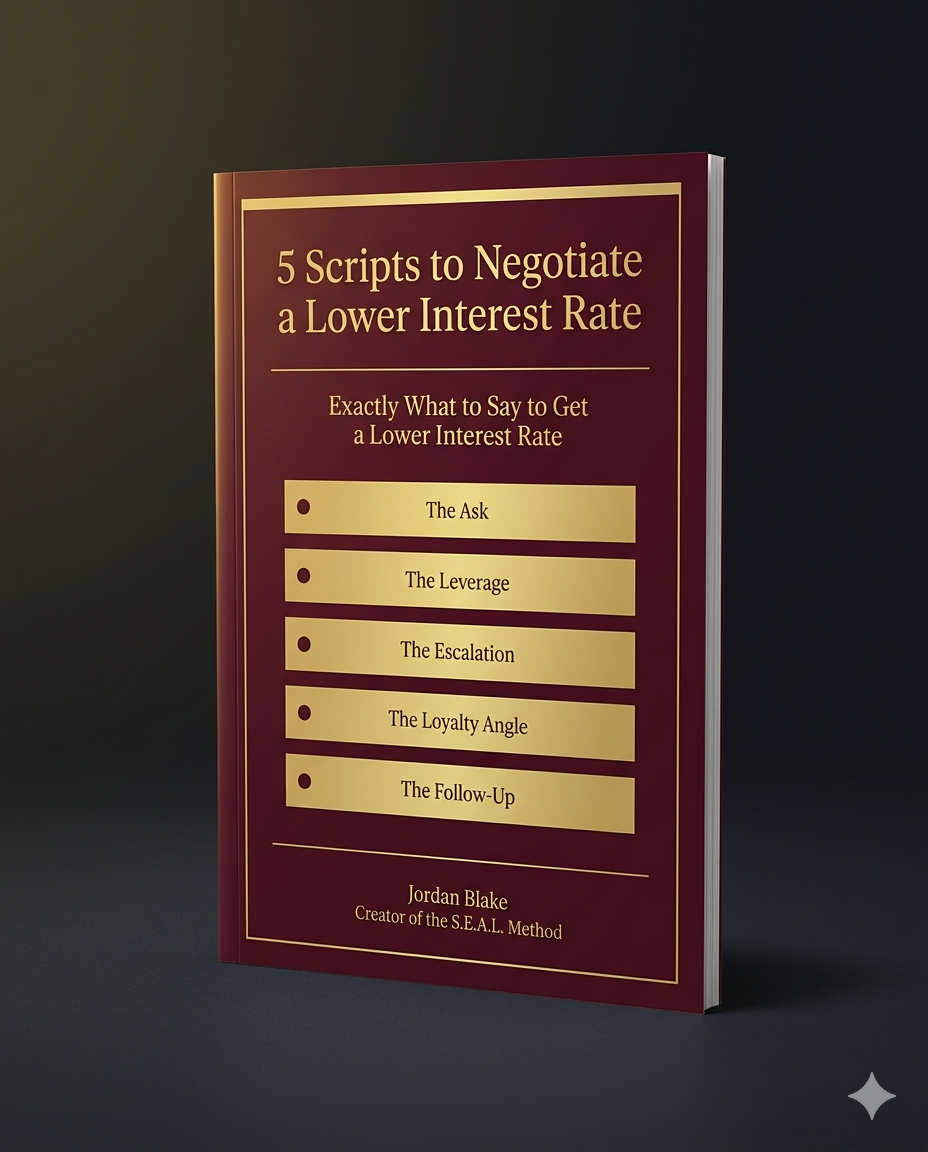

Bonus 2: 5 Scripts to Negotiate a Lower Interest Rate

Word-for-word scripts to call your credit card company and ask for a lower rate — available only while bonus spots remain.

Still unsure? Here's my promise to you:

Try the S.E.A.L. Method for 30 days. If you don't feel more in control of your money, email me and I'll refund you in full — no questions asked.

The discounted price is only available to the first 100 buyers.